In the following text I am going to look at how the Insurance Industry might develop in the coming years until 2030. Some of the topics, I think, will develop in the same way as it would for the banking industry. So please have a look at this blog entry.

Executive Summary

Choosing a business model for insurances is as difficult in the next few years as it is for banks but probably even more so. And how do those decisions influence and are influenced by the underlying IT? The following topics will be the focus areas:

- Strengthening partner ecosystem by concentrating on competitive advantages

- More and more services are being offered as SaaS. Taking advantage of reduced costs of this non competitive part of their business allows the insurance company so that their partly aging workforce can concentrate on creating new products and offerings. A clear strategy with a supporting API Management platform is needed to build a successful environment.

- More and more services are being offered as SaaS. Taking advantage of reduced costs of this non competitive part of their business allows the insurance company so that their partly aging workforce can concentrate on creating new products and offerings. A clear strategy with a supporting API Management platform is needed to build a successful environment.

- Flexible creation of new insurance offerings to address a dynamic market

- To support an easier creation of new offerings the IT environment needs to be able to implement changes dynamically. Building blocks coming from external partners and internal development need to be orchestrated using a container platform and an API management platform. Using such a platform will also enhance the choices where to deploy services on a (dedicated) public cloud or on premise.

- To support an easier creation of new offerings the IT environment needs to be able to implement changes dynamically. Building blocks coming from external partners and internal development need to be orchestrated using a container platform and an API management platform. Using such a platform will also enhance the choices where to deploy services on a (dedicated) public cloud or on premise.

- Sustainability will be one of the differentiating factors.

- Looking at the past weeks, news about climate change and the resulting problems are more and more frequent. Questions about what the “big” companies have done about this will be asked more and more. Especially companies in the financial services industry like pension funds etc. will be asked, as they have the ability to steer investments: “What have you done to avoid climate change?”. To evaluate what investments are sustainable is a complex problem. Here the open source idea can help to collaborate with other companies to consolidate necessary information, define metrics and implement processes. A strategy is needed to obtain necessary data and use it to decide viable projects.

- Looking at the past weeks, news about climate change and the resulting problems are more and more frequent. Questions about what the “big” companies have done about this will be asked more and more. Especially companies in the financial services industry like pension funds etc. will be asked, as they have the ability to steer investments: “What have you done to avoid climate change?”. To evaluate what investments are sustainable is a complex problem. Here the open source idea can help to collaborate with other companies to consolidate necessary information, define metrics and implement processes. A strategy is needed to obtain necessary data and use it to decide viable projects.

- Loyalty and Trust as the main currency of the future

- With Open Finance the need to openly share customer information rises. Choosing to be an intermediary or concentrating on providing insurance contracts will be a difficult question to answer. To broaden the ability to cross- and upsell, personalized offerings are needed. And for that you need the customer information. But only when the customers trust the insurance company will they share that information. To get a complete picture of the activity and preferences of a customer the position as intermediary is best suited. Focusing on the customer with AI, Automation and Digitalization will help to foster loyalty and trust.

As a result insurance companies should in the coming years focus to establish the following:

- a clear and focused cloud strategy to decide how to implement governance, security and placement of services.

- an api management system to integrate external partners and be integrated by others.

- a container platform to supply the basis for a dynamic placement of components with regards to cost, compliance and environmental requirements like GPU usage.

- an automation strategy spanning the entire services of the insurance to free up scarce workforce to concentrate on creating new services fit to address the dynamic market.

Strengthening partner ecosystem by concentrating on competitive advantages

In the future more focus needs to be placed on creating new and differentiating offerings for customers. As the workforce is aging and new employees are hard to find, the focus needs to be to remove the burden of keeping the lights on. Within each company the first focus is on automating repetitive work. Only a consolidated automation strategy over all services and departments will reap the full benefits. Deploying an application into an infrastructure needs several departments to collaborate. The experts on a given topic like networking or database administration can create automation scripts for all others to incorporate into meta tasks like deploying an application. With those freed up employees it is possible to focus on removing dependencies on outdated infrastructure and applications. Here the availability of experts is limited and in the coming years will be even scarcer. Again a reason to focus on automating. With the migration of services to new applications comes the freedom to enhance the functionality into a micro services based environment to foster a flexible platform. If then by choice or by necessity no more internal resources are available Software as a Service comes into play. The focus of SaaS will be the non differentiating tasks like providing Embedded Insurance or claims settlement and for example for car insurance providing add-on services like repairing the car in an authorized workshop.

But those services need governance and several questions need to be answered:

- How does the interaction work? What interfaces need to be filled?

- How is security handled ( with a focus on Supply Chain Security)?

- How are regulatory requirements like data privacy handled?

- What SLAs do those services have?

- How many transactions can they handle per second?

It is necessary to implement a governing body/department to choose the best fit for the company and then afterwards to acquire all of the answers from the chosen cloud service providers.

Integrating SaaS will be an essential part of the day to day business of an insurance company and must be organized. The integration of those services must be flexible. This adds the need for API management.

Flexible creation of new insurance offerings to address a dynamic market

The world around us is getting more dynamic every day. Opportunities appear and vanish. To participate in this “new normal” insurances need to create fitting offerings dynamically and roll them out to their existing and new customers. Long Term analysis of market chances might be too long to participate in a specific use case. So there are some areas where the result may not be 100% foreseeable. Is the infrastructure prepared to handle the requests? How much does it cost to create that new offering? How long will it take to develop? Like how successful is it going to be?

Goal will be to define a set of building blocks which can be reused and orchestrated dynamically. These building blocks can consist of inhouse services and external services. The IT infrastructure needs to support this strategy by supplying frameworks and environments which can be dynamically assembled and can grow. Looking at the current market development and the future prospects a container based platform is needed. Combining these building blocks necessitates interaction standards and a catalog of available services. Depending on the size and usage of this flexible framework a marketplace will be used to find fitting services.

Once the components of the new offering are defined several IT related areas have to be clarified:

- How do you access the services?

- How do the services interact with each other?

- Can the platform handle peaks?

- How is the orchestration done?

- How do I integrate legacy services?

To access the services in an easy, flexible and secure way API management is needed. This can also be used if the company decides to offer services to other market participants like for example appraisal of Art. An included payment mechanism is necessary. When integrating external services Secure Supply Chain becomes a concern. In the next few years implementing a Secure Supply Chain will become a central focus area. It can be seen that technical solutions are being created / implemented right now through for example a SBOM ( Software bill of materials).

Look at these links for more information:

- https://www.redhat.com/en/blog/sigstore-open-answer-software-supply-chain-trust-and-security

- https://www.linuxfoundation.org/blog/spdx-its-already-in-use-for-global-software-bill-of-materials-sbom-and-supply-chain-security/

As expected performance and usage is one area of vagenous a platform is needed for inhouse services which can handle varying numbers of requests and can dynamically react. Here on the one hand the API management comes into play to restrict this number of interactions per service and wrap the access to easily exchange implementations and internal processes. And on the other hand a container platform offers the flexibility to create new instances on the fly. Especially in the regulated industry the pain of moving applications between different clouds will increase with coming regulatory requirements. Here concepts like a trusted execution environment (TEE) will be implemented to allow moving the application between clouds while each cloud creates a secure environment for the applications to run in.

To still be able to handle requests exceeding the performance boundaries of the backend systems and services implementing streaming services will build a buffer for extraneous requests.Also a container platform offers through a service mesh the option to dynamically orchestrate micro services. Some of the services needed to implement the new offering will probably reside within legacy applications. Sometimes those are rather tending to be monolithic or written in a system which cannot be easily or not at all moved to a container platform. In the coming years an easy integration within the same platform will be essential. Combining Container and Virtual Images in one platform helps reduce the burden on the operational processes.

Sustainability will be one of the major differentiating factors

The world climate report was published at the beginning of this year. ( https://www.ipcc.ch/report/ar6/wg2/ ) The picture is dim. In 3 years time the output of carbon emissions worldwide needs to be turned around and reduced. In 8 years we need to reduce them by 45%. If this comes true we will probably be able to avoid the 1,5 degrees rise in temperatures. But this result needs not only the reduction of emissions but also actively removing carbon from the atmosphere.

This worldwide major undertaking can only be reached with a combined and collaborative effort of all countries and within each country all companies and people. The effects of extreme weather conditions resulting from climate change can be felt in every part of this world. For example, looking at India’s current heatwave where the temperature (>60° C near ground) is so high that plants cannot be grown anymore and that people cannot work to earn their livelihood. If this is not stopped and turned around it will lead to a migration wave out of uninhabitable regions causing conflicts and economic turmoil.

Therefore changing to a sustainable economy needs investing in the right places with the right budget. The FSI industry is a key player in those decisions. But how to evaluate the impact of an investment? What is the right project to finance? For this you need data and fitting models. Gathering that data is an enormous undertaking. A single company will have difficulties accomplishing this. Only in a collaborative effort can the information be obtained, pruned and maintained. Each participant in this community will invest work into this project and harvest benefits from it. This is exactly what Open Source is about. The goal of the OS Climate project ( https://os-climate.org/ ) is to establish a community of people, companies and organizations who will create datasets and models. The outlook that the global community will avoid the 1,5 °C goal is in my opinion unlikely. This will lead to questions about what each of the major players in this endeavor has done to help. Actively participating will lead to establishing the company as a responsible, trustworthy player.

Loyalty and Trust as the main currency of the future

When I compare my personal interactions with my insurances. The interactions with my insurance providers are very rare. For some I do not even remember their name. Other than the first time I signed the contract I didn’t have any interactions with them. Once a year I see that they have collected my yearly fee via direct debit. But that is it. So what are my parameters to decide which insurance to have a contract with? For me mostly the price. As more and more think in the same direction the margins of insurance contracts will be reduced dramatically. But how to grow the revenue stream to replace this?

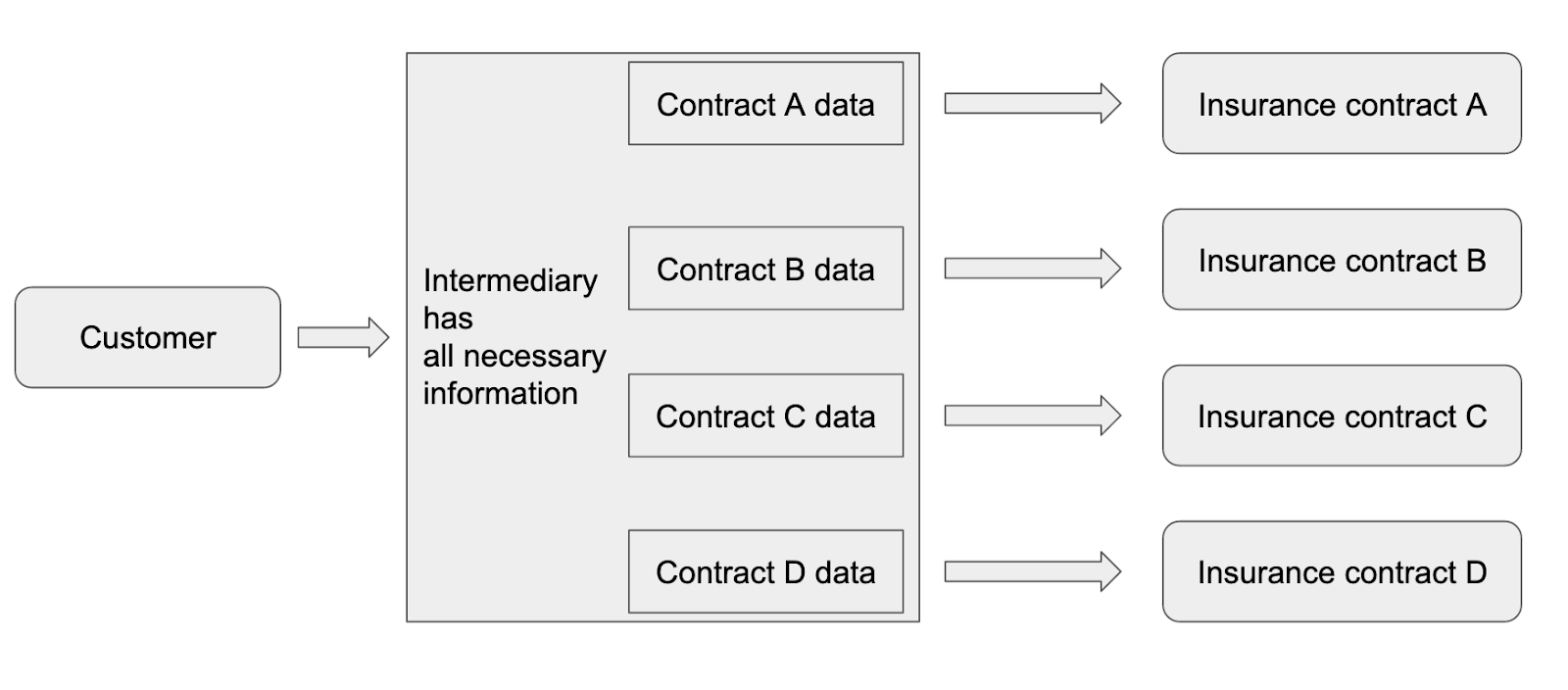

One of the reasons why it is easier for customers to find “cheaper” insurance are the comparison websites. The availability of those sites and services provided will increase in the future because of the need to open customer information to other market participants as it is for Banking in PSD2. There is legislation on the way which will force insurance companies to also make that information accessible. This opens up the market for intermediaries to consolidate all of the customers insurance business into one front end.

The flow of information is not distributed equally. The intermediary only needs to distribute the bare minimum of information to the insurance. All add-on information stays at the intermediary together with all the benefits from that information.

The insurance company now has to decide which way they would like to go:

- remain in the insurance provider market

- or become an intermediary.

Choosing to stay in the market solely as a provider will reduce margins with a uniform set of offerings. The web sites like Check24 will limit the set of parameters to compare the available contracts. Add-on services or niche features will not yield more revenue per contract as they are not easily visible on those result lists. And as the price will be the major decision point those add on options will not easily be visible for potential customers. So remaining in this space means diminishing margins where revenue needs to come from a higher volume of contracts.

Trust is at the core of the connection between customer and intermediary. Only when the customers trust the insurer, they willingly share more information than needed to get a better portfolio of contracts which fits their requirements. This is the major advantage of being the intermediary but also the major obstacle to becoming an intermediary. But for existing customers of the insurance this is already established. They can reuse this to grow their business with the customer.

This established trust can be used to gather more information to create a set of cross and upsell opportunities. With the database of all of their customers and through Open Finance they can better create offerings targeted at specific customer segments to acquire new customers. As a prerequisite the insurance company needs to be able to integrate in different systems and different interfaces. An API management system is needed to dynamically access the customers contracts from other market participants.

Growing trust and loyalty needs to be the central point in an ongoing relationship between customer and intermediary. The experience the customer has in those rare interactions, in my case almost none, with the insurance needs to be flawless. Timely responses, user friendly applications and easy claims handling is at the core. For example is claims regulation one of the most important interactions with the insurance so speedy claims regulation is needed. This needs to be done without sacrificing safe procedures. An AI supported fraud detection and claims regulations service will be enabled targeting at least for the first incident to guarantee a fast settlement.

To further increase the positive experience a full service option will be added. This would mean for example adding services provided by a local service provider who will take over the necessary steps in the claims process. Starting from the support right after an accident, to alerting police etc. supporting the customer at the site by delivering a replacement car directly to the customer, transporting the damaged car to an authorized workshop, repairing the car and then returning the repaired car to the owner at home or at his workplace. For this a platform for handling the automated processes has to be implemented using an API management platform to interact with the different regional service providers.

Being the intermediary opens up new opportunities for insurances with the foundation to build on with an already established relationship.

Summary

Looking at the different options to focus development on several major tasks need to be addressed in the coming years to prepare for this change.

- A clear cloud strategy

- An api management system to handle internal and external interactions

- A container platform to build a flexible base for all services

- A company wide automation platform to free up the reduced or retired workforce to create new and amazing offerings for customers

Together those 4 strategic decisions will open up new business opportunities and ensure remaining strong revenue streams.